The best life insurance policy is essential for protecting your family’s financial future. Life is unpredictable, and having the right coverage ensures your loved ones are supported in case of unexpected events. Whether it’s covering daily expenses, debts, or long-term goals, choosing a reliable policy provides peace of mind. Policy types, coverage options, and premiums help you select the most suitable plan for your needs and budget.

Life is unpredictable, and one of the best ways to prepare for uncertainties is through life insurance. Think of it as a safety net, not for you, but for your loved ones. When you’re gone, your family may still have bills, mortgages, tuition fees, or even just daily living expenses. Without a proper plan, all of that responsibility could suddenly fall on them. Life insurance steps in here, acting as a financial cushion that provides security, peace of mind, and stability for those who depend on you.

Why Life Insurance is Essential in Today’s World

We live in a world where financial commitments are increasing faster than incomes. Mortgages, student loans, car payments, and credit card debts have become part of everyday life. Add to that the rising cost of education and healthcare, and it becomes clear why life insurance is more relevant than ever.

Imagine a young couple with two children and a mortgage. If the primary breadwinner suddenly passes away, the surviving spouse could be left with not only emotional trauma but also financial devastation. Life insurance ensures that the children’s education continues, the house remains theirs, and daily needs don’t become a struggle.

Life insurance also serves as a tool for wealth building and tax planning. Some policies allow savings accumulation, while others provide cash value benefits that can be borrowed against in emergencies. In short, it’s not just about death benefits; it’s about providing financial freedom and flexibility during your lifetime, too.

Common Misconceptions About Life Insurance

Despite its importance, myths and misunderstandings often stop people from buying life insurance. Some common misconceptions include:

-

“I’m young, so I don’t need life insurance.” The truth is, the younger and healthier you are, the cheaper your premiums. Waiting until later means higher costs or even denial of coverage due to health issues.

-

“It’s too expensive.” Many overestimate the cost of life insurance. A basic term policy for a young, healthy individual can be surprisingly affordable.

-

“My employer’s insurance is enough.” Employer-provided life insurance often offers limited coverage—sometimes just one or two times your salary. That’s rarely sufficient for long-term needs.

-

“I don’t have dependents, so I don’t need it.” Even if you don’t have children or a spouse, insurance can cover debts, funeral expenses, or provide a legacy to loved ones or charity.

By clearing up these misconceptions, it becomes easier to see why life insurance isn’t just a “nice-to-have” but a “must-have” for almost everyone.

The Basics of Life Insurance

Before diving into how to get the best life insurance policy, you need to understand what life insurance is and how it functions. At its core, life insurance is a contract between you and the insurance company. You pay premiums, and in return, the insurer promises to pay your beneficiaries a lump sum (called the death benefit) upon your passing.

This agreement provides a financial safety net for your loved ones, helping them handle immediate and long-term expenses. Depending on the type of policy, life insurance can also serve as a financial planning tool during your lifetime.

What is Life Insurance?

Life insurance is essentially about risk management. It transfers the financial risk of your premature death from your family to an insurance company. By paying relatively small amounts (premiums) regularly, you protect your loved ones from facing potentially devastating financial losses.

Unlike other types of insurance, such as auto or health insurance, life insurance isn’t about protecting an asset but about protecting people. It ensures that your dependents can maintain their standard of living even if your income is no longer there.

Types of Life Insurance Policies

Life insurance isn’t one-size-fits-all. There are different types of policies designed for different needs and financial goals. The four primary categories are:

-

Term Life Insurance – Provides coverage for a specific period (10, 20, 30 years). Affordable but has no cash value.

-

Whole Life Insurance – Offers lifelong coverage with a guaranteed death benefit and cash value accumulation. Premiums are higher but stable.

-

Universal Life Insurance – Flexible premium payments and death benefits with investment opportunities.

-

Variable Life Insurance – Combines insurance with investment accounts, allowing growth but with higher risk.

Each of these options has pros and cons, which we’ll explore later in detail.

How Life Insurance Works

The basic mechanism of life insurance is straightforward:

-

You choose a policy and coverage amount.

-

You pay regular premiums (monthly, quarterly, or annually).

-

If you pass away while the policy is active, the insurer pays your beneficiaries.

For permanent policies, part of your premiums may go toward building cash value, which you can borrow against or withdraw. This makes some life insurance policies act like a hybrid of protection and investment.

Assessing Your Life Insurance Needs

Knowing you need insurance is one thing; figuring out how much you need is another. Buying too little means your family may struggle financially, while buying too much could strain your budget unnecessarily.

The right coverage depends on your lifestyle, debts, income, and dependents. You need to balance affordability with adequate protection.

Determining How Much Coverage You Need

A common rule of thumb is to get coverage equal to 10–15 times your annual income. But this is just a starting point. For example, if you earn $60,000 a year, you might consider coverage between $600,000 and $900,000.

However, every family’s needs are different. You should also factor in:

-

Outstanding debts (mortgage, car loans, student loans)

-

Future expenses (college tuition, weddings, retirement for your spouse)

-

Day-to-day living costs (groceries, bills, healthcare)

Using an online life insurance calculator can help fine-tune these numbers.

That Influence Coverage Amount

When calculating how much insurance you need, consider:

-

Dependents: The more people rely on your income, the higher the coverage should be.

-

Income Replacement: Think about how long your family will need your income to be replaced—until your children graduate? Until your spouse retires?

-

Existing Assets: If you already have savings, investments, or other insurance, you may need less coverage.

-

Inflation: Remember, the cost of living will rise in the future, so plan accordingly.

Short-Term vs. Long-Term Needs

Not all insurance needs are permanent. For example, if you just bought a 30-year mortgage, a term life policy for the same length might be ideal. On the other hand, if you want to leave an inheritance or support lifelong dependents, permanent insurance could be better.

Comparing Different Types of Life Insurance Policies

Choosing between term, whole, universal, and variable life insurance can feel overwhelming. Each type has unique features, benefits, and drawbacks. Understanding these differences is crucial to making the best choice.

Pros and Cons of Term Life Insurance

Pros:

-

Affordable premiums

-

Simple and easy to understand

-

Flexible term lengths (10, 20, 30 years)

Cons:

-

Coverage ends after the term expires

-

No cash value

-

Renewal premiums can be very high

Term insurance is best if you want high coverage at a low cost during your working years.

Pros and Cons of Whole Life Insurance

Pros:

-

Coverage lasts a lifetime

-

Cash value grows over time

-

Premiums remain fixed

Cons:

-

Higher premiums compared to term insurance

-

More complex policies

-

Cash value growth is usually conservative

Whole life is suitable for people who want lifelong protection plus a savings component.

Hybrid and Customizable Insurance Options

Modern insurance companies also offer hybrid products that combine features of different types. For example, you can have a term policy with an option to convert into whole life later. Some universal life policies allow flexible premiums, letting you adjust based on your financial situation.

How to Choose the Right Insurance Provider

The best policy isn’t just about the numbers; it’s also about the company you choose. After all, you’re trusting them with your family’s future.

Factors to Consider When Selecting a Company

When choosing an insurer, look beyond the price tag. Ask yourself:

-

How long has the company been in business?

-

Do they have a strong reputation for paying claims?

-

Are their policies flexible and transparent?

A good insurance provider should offer competitive pricing without sacrificing reliability.

Importance of Financial Strength Ratings

Insurance companies are rated by agencies like A.M. Best, Moody’s, and Standard & Poor’s. These ratings reflect a company’s financial stability and ability to pay claims. Always choose insurers with strong ratings, ideally “A” or higher.

Customer Service and Claim Settlement Ratio

A cheap premium won’t mean much if your family struggles to get the payout. Look for companies with high claim settlement ratios, which indicate they pay most claims promptly. Also, check customer reviews and the quality of their support services.

Comparing Premiums and Coverage Options

When it comes to life insurance, the balance between premiums (what you pay) and coverage (what your family receives) is the heart of the decision-making process. Many people make the mistake of either overpaying for coverage they don’t really need or underestimating how much protection their family requires. Striking the right balance ensures you stay financially comfortable while safeguarding your loved ones.

How Premiums are Calculated

Premiums aren’t set randomly; they’re calculated based on a mix of factors:

-

Age: The younger you are, the lower your premiums. A 25-year-old will pay significantly less than a 45-year-old for the same coverage.

-

Health: Medical conditions, smoking habits, and even weight can impact premiums. Healthier individuals typically enjoy lower rates.

-

Occupation & Lifestyle: High-risk jobs (like firefighting or construction) and dangerous hobbies (like skydiving) often mean higher costs.

-

Policy Type & Term Length: Term insurance is cheaper upfront, while permanent policies with cash value features come with higher premiums.

-

Coverage Amount: Naturally, the more coverage you want, the more you’ll pay.

Insurance companies use underwriting processes, sometimes requiring medical exams, to determine risk and set your premium accordingly.

Balancing Affordability with Adequate Coverage

It’s tempting to go for the cheapest policy available, but affordability should never come at the cost of inadequate protection. Ask yourself: If I were gone tomorrow, would my family truly be financially secure with this amount of coverage?

Here are some strategies to keep premiums manageable without compromising coverage:

-

Buy life insurance as early as possible to lock in low rates.

-

Choose term life for temporary needs (like a mortgage or raising kids).

-

Combine a smaller permanent policy with a larger term policy for balance.

-

Improving your health, quitting smoking, losing weight, or managing conditions can lead to lower premiums.

Making Comparisons Between Policies

When comparing policies, always request multiple quotes. But don’t just look at the price tag, check the fine print:

-

Does the policy have flexible renewal or conversion options?

-

What riders (add-ons) are available, like critical illness or accidental death benefits?

-

Are there hidden fees or administrative charges in permanent policies?

The best life insurance policy is one that offers enough protection for your family while fitting comfortably into your budget.

Policy Riders and Add-Ons

Life insurance policies aren’t always rigid. Many insurers allow you to customize your plan with optional riders and add-ons that expand your coverage. Think of them as upgrades to a base model car, designed to suit your personal needs.

Popular Life Insurance Riders

Some of the most common riders include:

-

Accidental Death Benefit Rider: Provides an extra payout if you die in an accident.

-

Waiver of Premium Rider: Waives your premium payments if you become disabled and unable to work.

-

Critical Illness Rider: Pays a lump sum if you’re diagnosed with a serious illness like cancer or heart disease.

-

Child Term Rider: Offers temporary coverage for your children.

-

Return of Premium Rider: Refunds the premiums paid if you outlive your term policy.

Benefits of Adding Riders

Riders enhance your policy by covering gaps that standard policies may overlook. For example, a critical illness rider can act like a financial lifeline during a health crisis, while a waiver of premium rider ensures your policy doesn’t lapse if you’re unable to work.

When Riders Make Sense

Not all riders are necessary for everyone. Adding too many can significantly increase your premium. Riders make the most sense when they align with your specific risks. For instance:

-

If you work in a high-risk occupation, an accidental death benefit rider may be wise.

-

If your family has a history of major illnesses, a critical illness rider could be invaluable.

Choosing riders should be strategic, not impulsive.

The Role of Age and Health in Getting the Best Rates

Two of the most powerful factors in determining your life insurance premium are age and health. These elements can make the difference between an affordable policy and one that eats up a chunk of your budget.

Why Age Matters

Life insurance companies see younger applicants as lower risk since they’re statistically less likely to pass away during the policy term. That’s why a 30-year-old can lock in a 20-year term policy at a fraction of the cost compared to someone who waits until 45.

Pro tip: The best time to buy life insurance is always “now.” Waiting only increases your cost and, in some cases, reduces your eligibility.

The Impact of Health on Premiums

Insurers require medical information sometimes through exams, sometimes through questionnaires. They look at:

-

Medical history (chronic diseases, surgeries, family health background)

-

Lifestyle choices (smoking, drinking, exercise)

-

Current health indicators (blood pressure, cholesterol, BMI)

Smokers, for example, can pay two to three times more for life insurance compared to non-smokers.

How to Improve Your Insurability

Even if you’re not in perfect health, there are steps to lower your premiums:

-

Quit smoking and limit alcohol consumption.

-

Adopt a healthier lifestyle with exercise and a balanced diet.

-

Get regular checkups to manage and document improvements in your health.

-

Consider “no medical exam” policies if health issues make traditional insurance too costly, though these tend to have lower coverage limits.

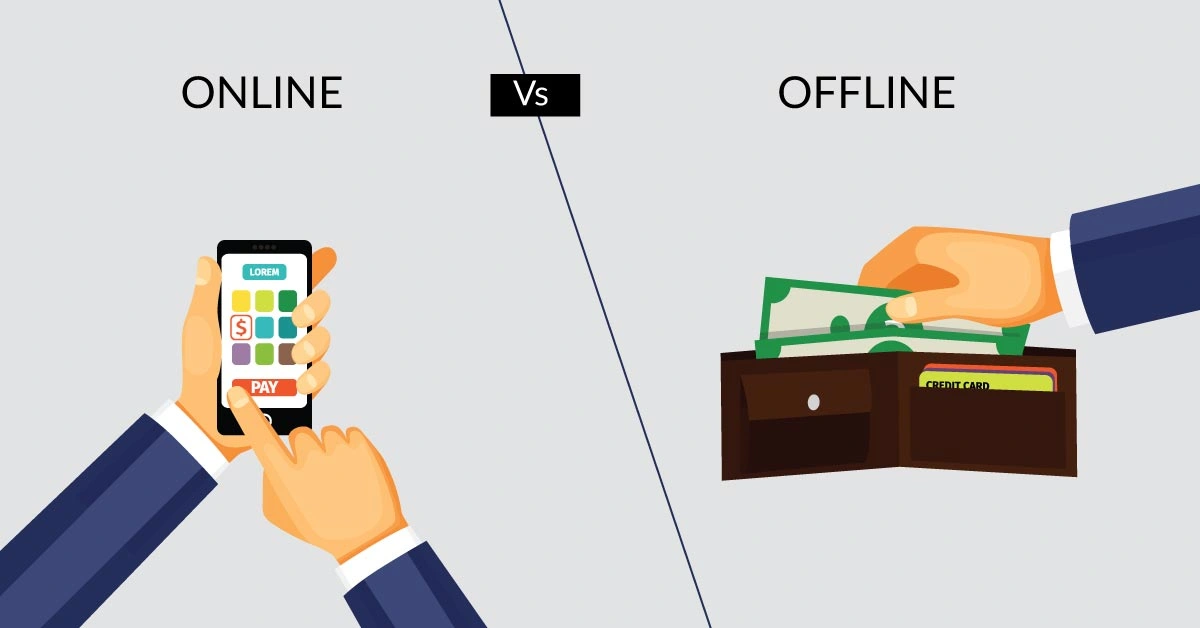

Online vs. Offline Life Insurance Buying: Which is Better?

Best life insurance policy. With digital platforms booming, buying life insurance online has become as easy as ordering groceries. But does that mean it’s always the better choice compared to traditional agents and offline methods? Let’s weigh both options.

Advantages of Buying Life Insurance Online

-

Convenience: Compare multiple policies and apply from your couch.

-

Lower Costs: Online insurers often have reduced administrative expenses, which can translate into lower premiums.

-

Transparency: Digital platforms make it easier to see side-by-side comparisons.

-

Speed: Some policies get approved instantly or within a few days.

Advantages of Buying Life Insurance Offline

-

Personal Guidance: An experienced agent can explain complex policies and help customize coverage.

-

Tailored Advice: Agents can assess your full financial situation and suggest policies that match your goals.

-

Relationship: Having a personal contact can make claims and adjustments easier.

Which One Should You Choose?

If you’re confident in doing research and know exactly what you need, buying online might be faster and cheaper. However, if you prefer detailed advice and want someone to walk you through the fine print, working with an agent offline could save you from costly mistakes.