How Does Travel Insurance Cover Pre-Existing Conditions: Travel insurance is a smart way to protect yourself from unexpected medical costs, trip cancellations, or delays. But if you have a pre-existing condition—like asthma, diabetes, or heart disease—you may wonder if you’re covered. The good news? Many U.S. travel insurance plans can cover pre-existing conditions, but there are rules.

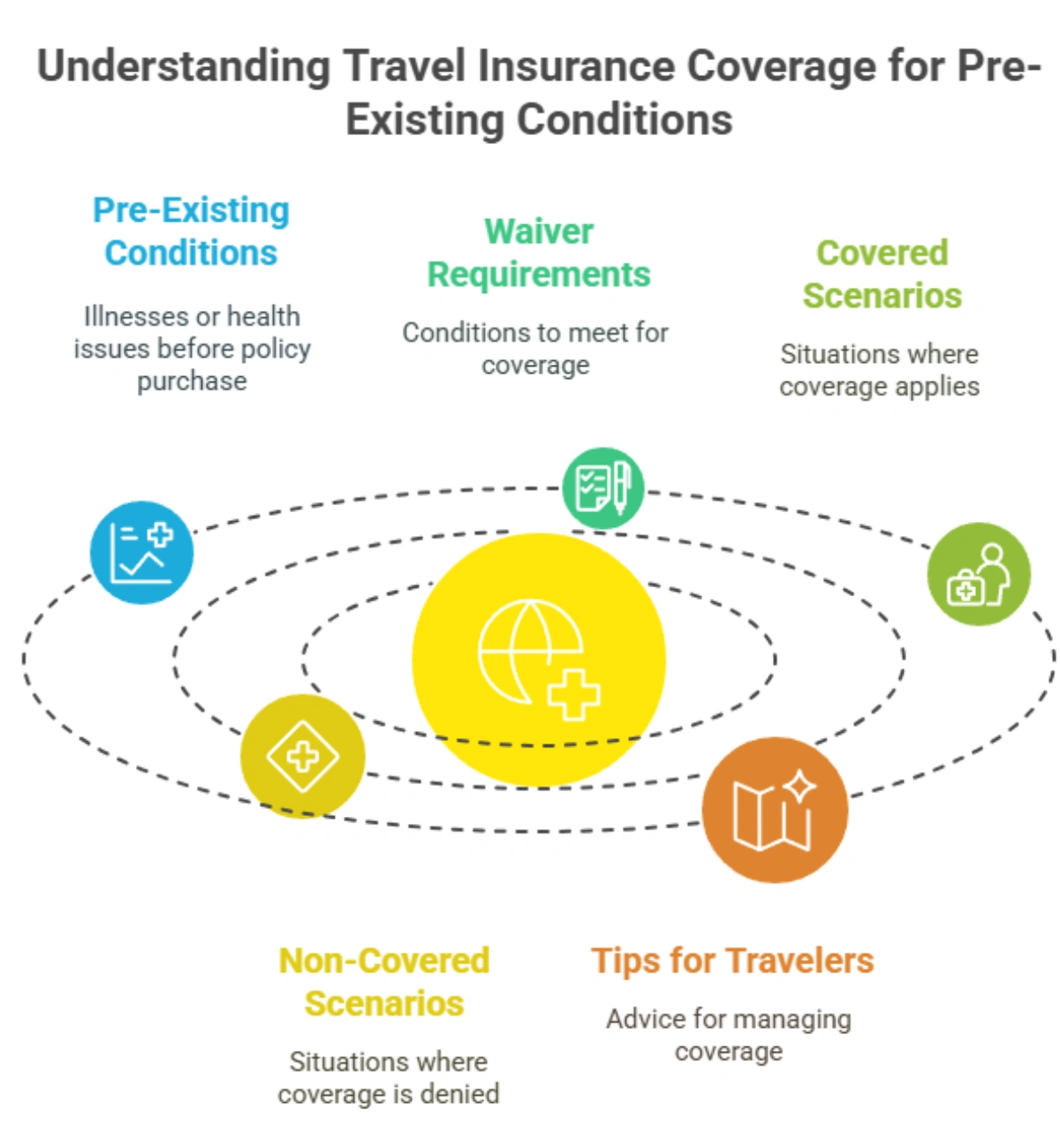

What Is a Pre-Existing Condition?

A pre-existing condition is any illness, injury, or health issue you had before buying your travel insurance policy. It could be something you were treated for or something you’re currently managing with medication.

Does Travel Insurance Cover It?

Yes, but coverage is not automatic. Most policies offer a waiver for pre-existing conditions, which means they’ll still cover medical issues related to your condition if you meet specific requirements.

Common Requirements for Coverage:

- Buy early – You usually need to purchase your plan within 14–21 days of making your first trip payment.

- Be medically stable – You must be stable (no recent changes in treatment or condition) for a certain period, often 60–180 days before the policy’s start.

- Insure full trip cost – You need to insure 100% of your prepaid, non-refundable trip expenses.

- Fit to travel – A doctor should not have advised against travel at the time of booking.

What’s Typically Covered?

With the waiver, you can be covered for:

- Emergency medical treatment

- Trip interruption or cancellation due to your condition

- Emergency evacuation

What’s Not Covered?

Without the waiver, any claim tied to your pre-existing condition might be denied. That includes hospital visits, medication, or trip cancellation because of a flare-up.

Tips:

- Always read the fine print.

- Ask the insurer if their plan offers a pre-existing condition waiver.

- Keep medical records handy in case you need to file a claim.

Traveling with a health condition doesn’t mean risking your trip. With the right plan and early action, you can explore with peace of mind.